Asset Replacement Analysis

Decision on whether an existing asset should be retired from use, continued in service, or replaced with a new asset.

Defender: An existing (old) asset.

Challengers: One or more alternative replacement (new) assets.

Factors to be concerned:

Recognition and acceptance of past errors

Ignorance of sunk costs

Opportunity cost of the defender (outsider viewpoint)

Economic life of the proposed challengers

Remaining economic life of the defender

Income tax considerations

Asset Lives

Physical Life: the time period that an asset is obsoleted from new.

Useful Life: the time period that an asset is kept in productive service (primary or backup).

Technical Life: the time period that an asset is no longer technologically advanced.

Depreciation Life: the time period that the book value of an asset is depreciated to zero.

Economic Life: the time period that an asset is not economically feasible to keep using it.

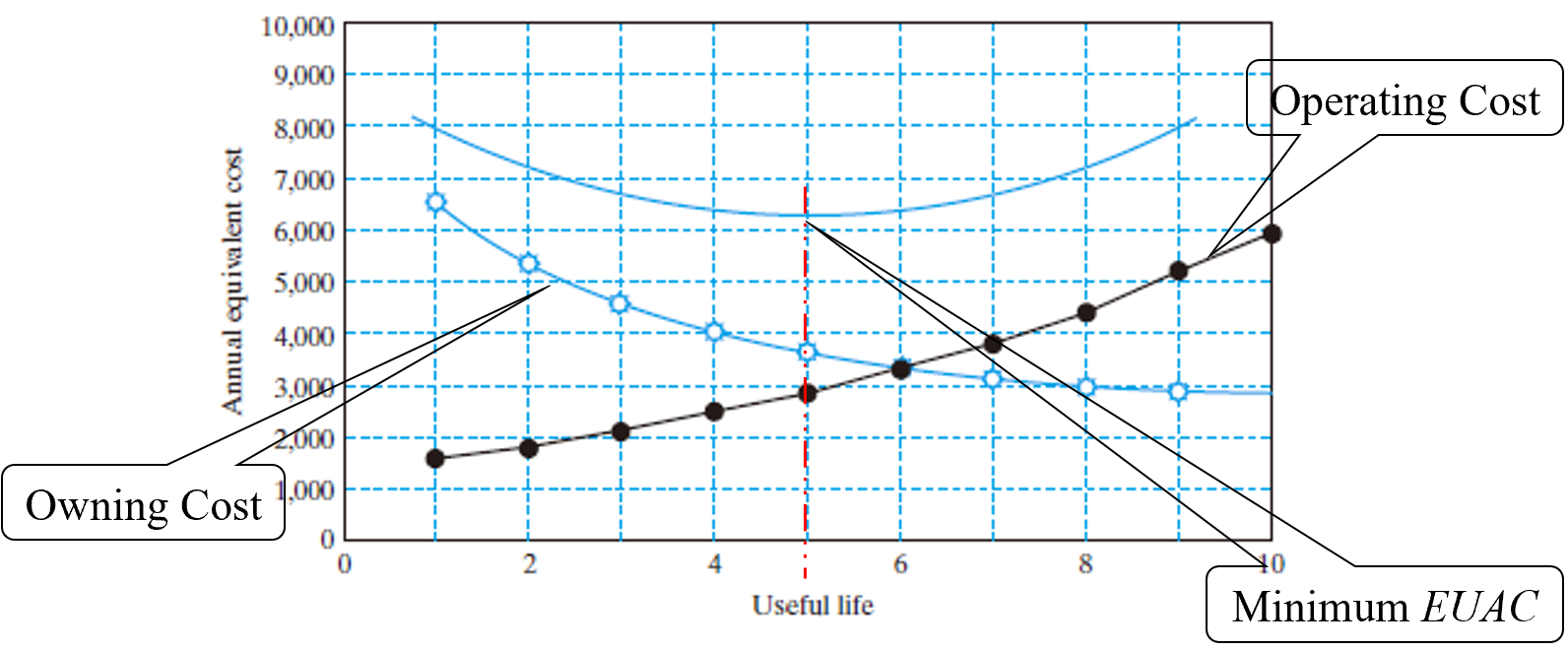

Equivalent Uniform Annual Cost (EUAC)

Annual equivalent cost of owning and operating an asset.

The time to yield minimum EUAC is the economic life.

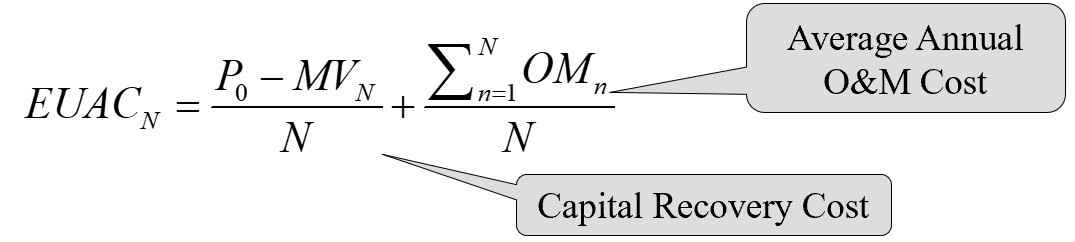

Without considering Time Value of Money

N — Useful life of the asset;

P0 — Initial investment of the asset;

MVN — Market value of the asset at the end of year N;

OMn — Operation and Maintenance cost of the asset in year n

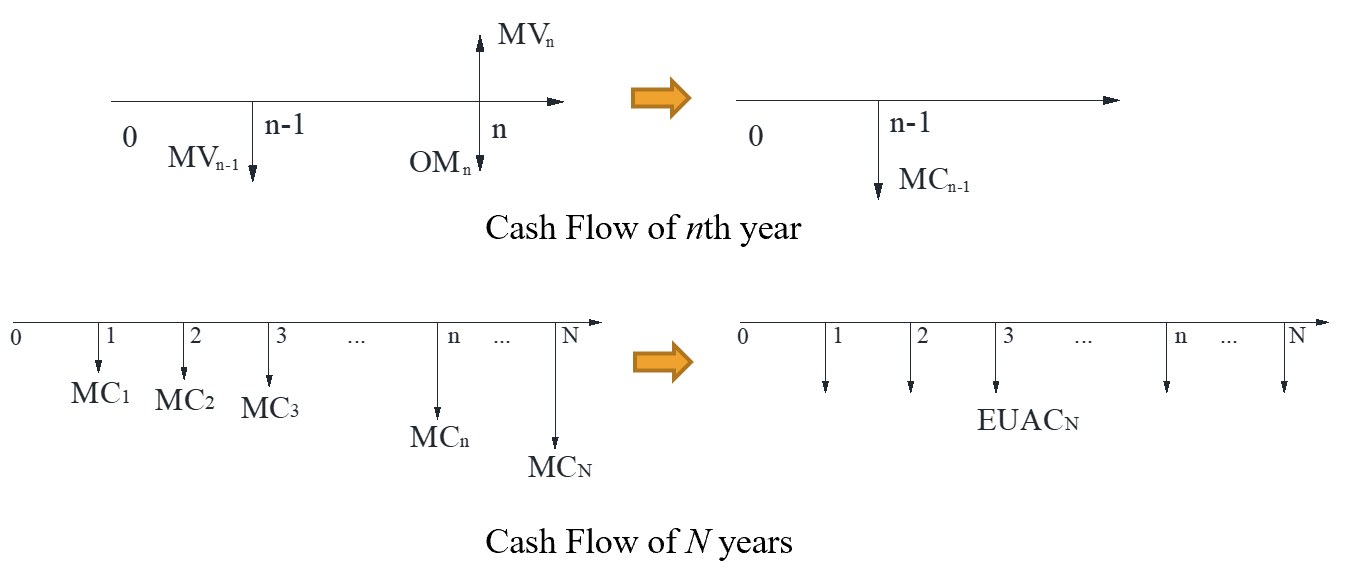

Considering Time Value of Money

![]()

MCn — Marginal cost of year n;

![]()

MVn — Market value of the asset at the end of year n;

OMn — Operation and maintenance cost of the asset in year n