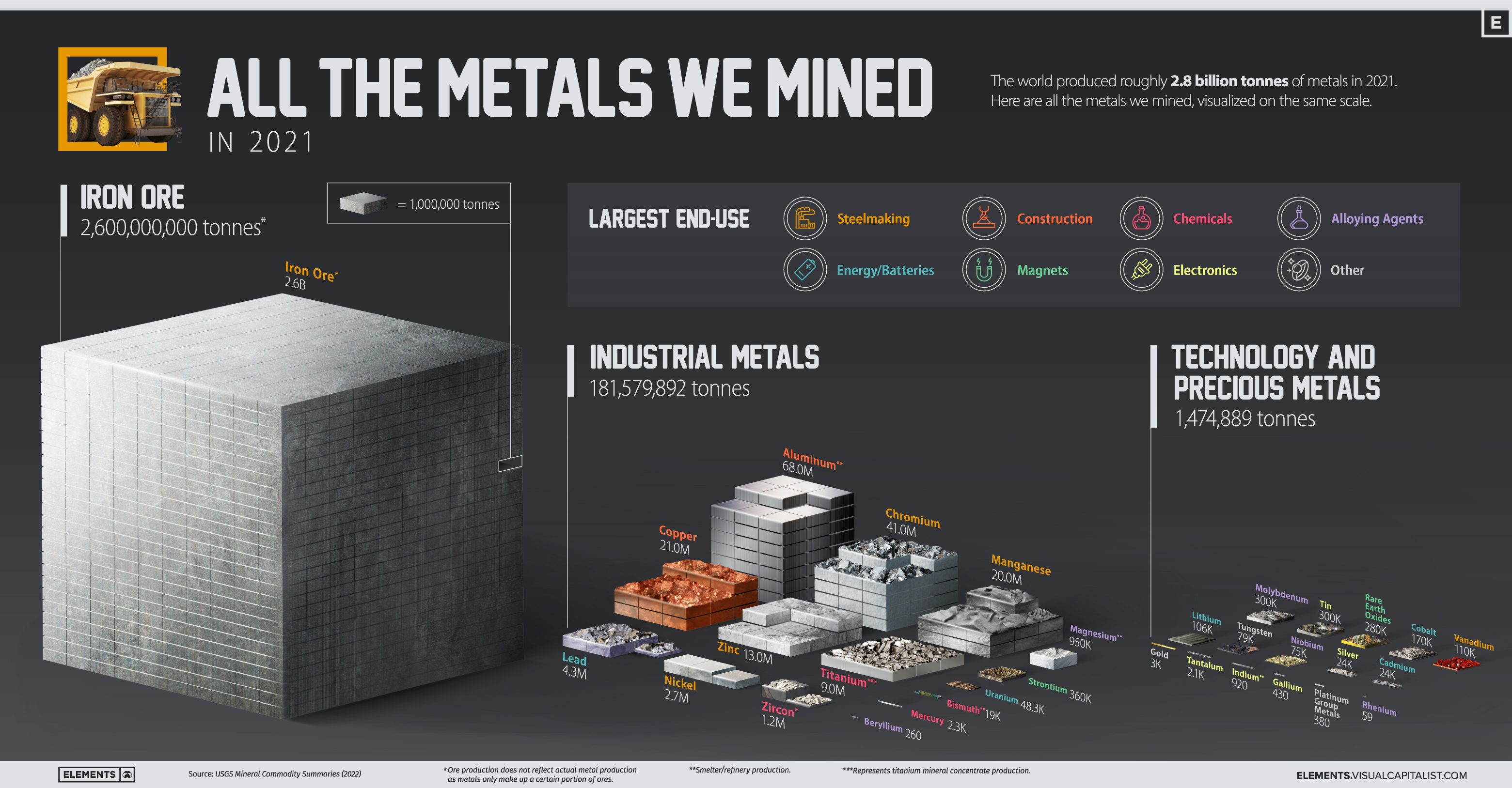

All the Metals We Mined in 2021

This was originally posted on Elements. Sign up to the free mailing list to get beautiful visualizations on natural resource megatrends in your email every week.

“If you can’t grow it, you have to mine it” is a famous saying that encapsulates the importance of minerals and metals in the modern world.

From every building we enter to every device we use, virtually everything around us contains some amount of metal.

The above infographic visualizes all 2.8 billion tonnes of metals mined in 2021 and highlights each metal’s largest end-use using data from the United States Geological Survey (USGS).

Why Do We Mine So Much Iron Ore?

Iron ore accounted for 93% of the metals mined in 2021, with 2.6 billion tonnes extracted from the ground. It’s important to note that this is ore production, which is typically higher than metal production since metals are extracted and refined from ores. For example, the iron metal content of this ore is estimated at 1.6 billion tonnes.

| Metal/Ore | 2021 Mine Production (tonnes) | % of Total |

|---|---|---|

| Iron ore | 2,600,000,000 | 93.4% |

| Industrial metals | 181,579,892 | 6.5% |

| Technology and precious metals | 1,474,889 | 0.05% |

| Total | 2,783,054,781 | 100.0% |

With 98% of it converted into pig iron to make steel, iron ore is ubiquitous in our lives. Steel made from iron ore is used in construction, transportation, and household appliances, and it’s likely that you encounter something made out of it every day, especially if you live in a city.

Due to its key role in building infrastructure, iron ore is one of the most important materials supporting urbanization and economic growth.

Industrial Metals

Industrial metals are largely used in steelmaking, construction, chemical manufacturing, and as alloying agents. In 2021, the world mined over 181 million tonnes of these metals.

| Industrial Metals | 2021 Mine Production (tonnes) | % of Total |

|---|---|---|

| Aluminum* | 68,000,000 | 37.4% |

| Chromium | 41,000,000 | 22.6% |

| Copper | 21,000,000 | 11.6% |

| Manganese | 20,000,000 | 11.0% |

| Zinc | 13,000,000 | 7.2% |

| Titanium (mineral concentrates) | 9,000,000 | 5.0% |

| Lead | 4,300,000 | 2.4% |

| Nickel | 2,700,000 | 1.5% |

| Zirconium Minerals (Zircon) | 1,200,000 | 0.7% |

| Magnesium* | 950,000 | 0.5% |

| Total | 181,579,892 | 100.0% |

Showing 1 to 10 of 15 entries

*Represents refinery/smelter production.

Aluminum accounted for nearly 40% of industrial metal production in 2021. China was by far the largest aluminum producer, making up more than half of global production. The construction industry uses roughly 25% of annually produced aluminum, with 23% going into transportation.

Chromium is a lesser-known metal with a key role in making stainless steel stainless. In fact, stainless steel is usually composed of 10% to 30% of chromium, enhancing its strength and corrosion resistance.

Copper, manganese, and zinc round out the top five industrial metals mined in 2021, each with its own unique properties and roles in the economy.

Technology and Precious Metals

Technology metals include those that are commonly used in technology and devices. Compared to industrial metals, these are usually mined on a smaller scale and could see faster consumption growth as the world adopts new technologies.

| Technology and Precious Metals | 2021 Mine Production (tonnes) | % of Total |

|---|---|---|

| Tin | 300,000 | 20.3% |

| Molybdenum | 300,000 | 20.3% |

| Rare Earth Oxides | 280,000 | 19.0% |

| Cobalt | 170,000 | 11.5% |

| Vanadium | 110,000 | 7.5% |

| Lithium | 106,000 | 7.2% |

| Tungsten | 79,000 | 5.4% |

| Niobium | 75,000 | 5.1% |

| Silver | 24,000 | 1.6% |

| Cadmium | 24,000 | 1.6% |

| Total | 1,474,889 | 100.0% |

Showing 1 to 10 of 16 entries

*Represents refinery/smelter production.

The major use of rhenium, one of the rarest metals in terms of production, is in superalloys that are critical for engine turbine blades in aircraft and gas turbine engines. The petroleum industry uses it in rhenium-platinum catalysts to produce high-octane gasoline for vehicles.

In terms of growth, clean energy technology metals stand out. For example, lithium production has more than doubled since 2016 and is set to ride the boom in EV battery manufacturing. Over the same period, global rare earth production more than doubled, driven by the rising demand for magnets.

Indium is another interesting metal on this list. Most of it is used to make indium tin oxide, an important component of touchscreens, TV screens, and solar panels.

The Metal Mining Megatrend

The world’s material consumption has grown significantly over the last few decades, with growing economies and cities demanding more resources.

Global production of both iron ore and aluminum has more than tripled relative to the mid-1990s. Other metals, including copper and steel, have also seen significant consumption growth.

Today, economies are not only growing and urbanizing but also adopting mineral-intensive clean energy technologies, pointing towards further increases in metal production and consumption.

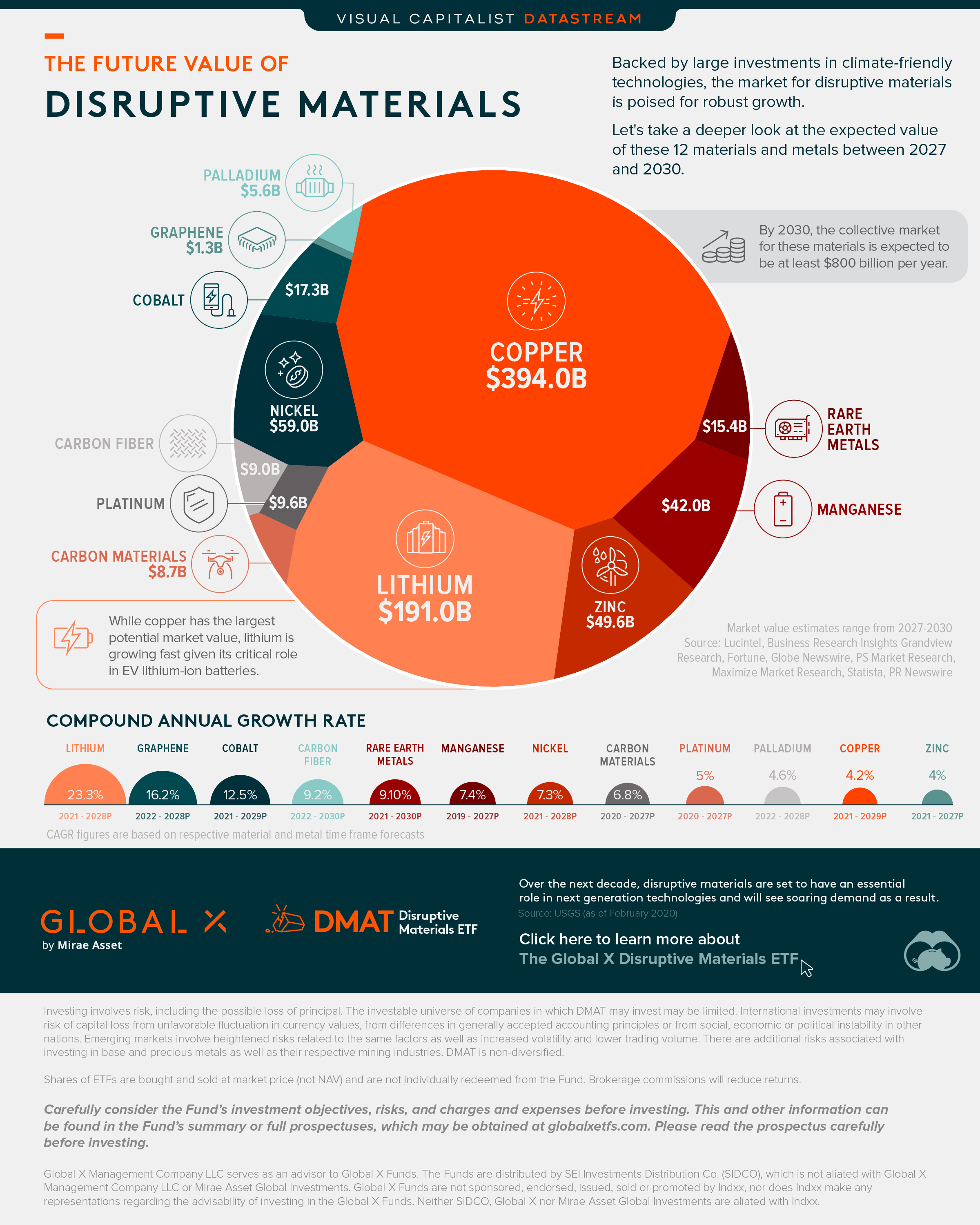

The Future Value of Disruptive Materials

The Briefing

By 2030, the collective market for disruptive materials is expected to reach over $800 billion

Copper is the largest market while lithium is the fastest growing

The Future Value of Disruptive Materials

A select number of materials have a critical role to play in the expansion of next generation technologies. This could lead to a surge in demand and a potential soaring of market values for each material as a result.

This graphic from Global X ETFs takes a closer look at the forecasted market value for 12 disruptive materials, which are seeing increasingly large climate investment.

Soaring Market Values

The materials highlighted are each a billion dollar market in their own right. But which has the largest projected future market value?

Copper is one of the largest and most mature markets from this group. And as a result sees a lower projected compound annual growth rate (CAGR).

However, when it comes to the fastest growing market, lithium reigns supreme with a CAGR of over 23% between the forecast period of 2021 and 2028. Lithium is a vital ingredient for lithium-ion batteries, used in EVs and elsewhere.

| Disruptive Material | Projected Market Value ($B) | CAGR (over forecast period) |

|---|---|---|

| Copper | $394.0B by 2029 | 4.2% (2021-2029P) |

| Lithium | $191.0B by 2028 | 23.3% (2021-2028P) |

| Nickel | $59.0B by 2028 | 7.3% (2021-2028P) |

| Zinc | $49.6B by 2027 | 4.0% (2021-2027P) |

| Manganese | $42.0B by 2027 | 7.4% (2019-2027P) |

| Cobalt | $17.3B by 2029 | 12.5% (2021-2029P) |

| Rare Earth Metals | $15.4B by 2030 | 9.1% (2021-2030P) |

| Platinum | $9.6B by 2027 | 5.0% (2020-2027P) |

| Carbon Fiber | $9.0B by 2030 | 9.2% (2022-2030P) |

| Carbon Materials | $8.7B by 2027 | 6.8% (2020-2027P) |

| Palladium | $5.6B by 2028 | 4.6% (2022-2028P) |

| Graphene | $1.3B by 2028 | 16.2% (2022-2028P) |

Altogether, the collective market value for these top materials is expected to be worth over $800 billion by the end of the decade. And in the subsequent years, as efforts to tackle climate change accelerate, the collective value of these materials may well hit $1 trillion.

Should You Invest in Disruptive Materials?

Should You Invest in Disruptive Materials?

New technologies are having a transformative impact on the transportation and energy sectors. As these technologies develop, it is becoming clear that a small selection of materials, metals, and minerals—known collectively as disruptive materials—are critical components required to innovate.

This graphic from Global X ETFs takes a closer look at the disruptive materials that are key to fueling climate technologies. With a growing global effort to decarbonize, disruptive materials may enter a demand supercycle, characterized as a structural decades-long period of rising demand and rising prices.

Building Blocks Of the Future

There are 10 categories of disruptive materials in particular that are expected to see demand growth as part of their role within emerging technologies.

| Disruptive Material | Applicability |

|---|---|

| Zinc | Protects metal surfaces from rusting through a process called galvanization. This is essential to wind energy. |

| Palladium & Platinum | Often used in catalytic converters, thus playing a major role in hydrogen fuel cell technology. |

| Nickel | A corrosion-resistant metal used to make other metals more durable. |

| Manganese | An important mineral needed for battery and steel production. |

| Lithium | The foundational component of lithium-ion batteries. |

| Graphene | The thinnest known material which is also 100x stronger than steel. Used in sensors and transistors. |

| Rare Earth Materials | A broader category including 15 lanthanide series elements, plus yttrium. These metals are found in all types of electronics. |

| Copper | A reliable conductor of electricity. It can also kill bacteria, making it useful during pandemics. |

| Cobalt | An important ingredient for rechargeable lithium batteries, found only in specific regions of the world. |

| Carbon Fiber & Carbon Materials | Strong and lightweight materials with applications in aerospace and the automotive industry. |

While these 10 categories do not make up the entire disruptive material universe, all are essential to securing a climate and technologically advanced future.

How The Green Revolution Is Transforming the Materials Market

The data on rising global temperatures and extreme weather events is jarring and has governments and organizations from all over the world ramping up efforts to combat its effects through new budgets and policies.

Take the soaring total number of U.S. climate disasters for instance. Most recently in 2021, the quantity of weather disasters stood at 20 whereas in 1980 it stood as a much smaller figure of three. In addition, total disaster costs have risen above $100 billion per year.

Globally, the top 10 most extreme weather events in 2021 racked up $170 billion in costs.

| Rank | Climate Event | Cost ($B) |

|---|---|---|

| #1 | Hurricane Ida | $65.0B |

| #2 | European floods | $43.0B |

| #3 | Texas winter storm | $23.0B |

| #4 | Henan floods | $17.6B |

| #5 | British Columbia floods | $7.5B |

| #6 | France’s “cold wave” | $5.6B |

| #7 | Cyclone Yaas | $3.0B |

| #8 | Australian floods | $2.1B |

| #9 | Typhoon In-fa | $2.0B |

| #10 | Cyclone Tauktae | $1.5B |

What’s more, some research estimates that these rising costs are far from coming to a halt. By 2050 the annual cost of weather disasters could surge past $1 trillion a year. In an effort to slow rising temperatures, governments are dramatically increasing their climate spending. For example, the U.S. is set to spend $80 billion annually over the next five years.

To see how climate spending impacts the materials market, consider the complexity behind a typical solar panel which requires almost 20 different materials including copper for wiring, boron and phosphorus for semiconductors, as well as zinc and magnesium for its frame.

Overall, these materials are essential to the expansion of a variety of emerging technologies like lithium batteries, solar panels, wind turbines, fuel cells, robotics, and 3D printers. And therefore, are translating to higher levels of demand for the disruptive materials that make combating climate change possible.

Estimated Disruptive Material Growth by 2040

A societal shift in how we address climate change is forecasted to lead to a demand supercycle for disruptive materials and acts as a massive tailwind.

But just how large is this expected level of demand to be? To answer this, we use two scenarios created by The International Energy Agency (IEA). The first is the Stated Policies Scenario, a more conservative model that assumes demand for material will double by 2040 relative to 2020 levels. Under this scenario, it’s assumed that society takes climate action in line with current and existing policies and commitments.

Then there is the Sustainable Development Scenario, which assumes more drastic action will take place to transform global energy use and meet international climate goals. Under this scenario, the demand for disruptive materials could rise as high as 300% relative to 2020 levels.

However, under both scenarios there’s still significant demand for each type of material.

| Disruptive Material | Stated Policies Scenario Demand Relative to 2020 | Sustainable Development Scenario Demand Relative to 2020 |

|---|---|---|

| Lithium | 13X | 42X |

| Graphite | 8X | 25X |

| Cobalt | 6X | 21X |

| Nickel | 7X | 19X |

| Manganese | 3X | 8X |

| Rare earth elements | 3X | 7X |

| Copper | 2X | 3X |

Overall, lithium is expected to see the most explosive surge in demand, as it could reach anywhere from 13 to 42 times the level of demand seen in 2020, based on the above scenarios.

Introducing the Global X Disruptive Materials ETF

The Global X Disruptive Materials ETF (Ticker: DMAT) seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the Solactive Disruptive Materials Index.

Investors can use this passively managed solution to gain exposure to the rising demand for disruptive materials and climate technologies.

Should You Invest in Disruptive Materials?

New technologies are having a transformative impact on the transportation and energy sectors. As these technologies develop, it is becoming clear that a small selection of materials, metals, and minerals—known collectively as disruptive materials—are critical components required to innovate.

This graphic from Global X ETFs takes a closer look at the disruptive materials that are key to fueling climate technologies. With a growing global effort to decarbonize, disruptive materials may enter a demand supercycle, characterized as a structural decades-long period of rising demand and rising prices.

Building Blocks Of the Future

There are 10 categories of disruptive materials in particular that are expected to see demand growth as part of their role within emerging technologies.

| Disruptive Material | Applicability |

|---|---|

| Zinc | Protects metal surfaces from rusting through a process called galvanization. This is essential to wind energy. |

| Palladium & Platinum | Often used in catalytic converters, thus playing a major role in hydrogen fuel cell technology. |

| Nickel | A corrosion-resistant metal used to make other metals more durable. |

| Manganese | An important mineral needed for battery and steel production. |

| Lithium | The foundational component of lithium-ion batteries. |

| Graphene | The thinnest known material which is also 100x stronger than steel. Used in sensors and transistors. |

| Rare Earth Materials | A broader category including 15 lanthanide series elements, plus yttrium. These metals are found in all types of electronics. |

| Copper | A reliable conductor of electricity. It can also kill bacteria, making it useful during pandemics. |

| Cobalt | An important ingredient for rechargeable lithium batteries, found only in specific regions of the world. |

| Carbon Fiber & Carbon Materials | Strong and lightweight materials with applications in aerospace and the automotive industry. |

While these 10 categories do not make up the entire disruptive material universe, all are essential to securing a climate and technologically advanced future.

How The Green Revolution Is Transforming the Materials Market

The data on rising global temperatures and extreme weather events is jarring and has governments and organizations from all over the world ramping up efforts to combat its effects through new budgets and policies.

Take the soaring total number of U.S. climate disasters for instance. Most recently in 2021, the quantity of weather disasters stood at 20 whereas in 1980 it stood as a much smaller figure of three. In addition, total disaster costs have risen above $100 billion per year.

Globally, the top 10 most extreme weather events in 2021 racked up $170 billion in costs.

| Rank | Climate Event | Cost ($B) |

|---|---|---|

| #1 | Hurricane Ida | $65.0B |

| #2 | European floods | $43.0B |

| #3 | Texas winter storm | $23.0B |

| #4 | Henan floods | $17.6B |

| #5 | British Columbia floods | $7.5B |

| #6 | France’s “cold wave” | $5.6B |

| #7 | Cyclone Yaas | $3.0B |

| #8 | Australian floods | $2.1B |

| #9 | Typhoon In-fa | $2.0B |

| #10 | Cyclone Tauktae | $1.5B |

What’s more, some research estimates that these rising costs are far from coming to a halt. By 2050 the annual cost of weather disasters could surge past $1 trillion a year. In an effort to slow rising temperatures, governments are dramatically increasing their climate spending. For example, the U.S. is set to spend $80 billion annually over the next five years.

To see how climate spending impacts the materials market, consider the complexity behind a typical solar panel which requires almost 20 different materials including copper for wiring, boron and phosphorus for semiconductors, as well as zinc and magnesium for its frame.

Overall, these materials are essential to the expansion of a variety of emerging technologies like lithium batteries, solar panels, wind turbines, fuel cells, robotics, and 3D printers. And therefore, are translating to higher levels of demand for the disruptive materials that make combating climate change possible.

Estimated Disruptive Material Growth by 2040

A societal shift in how we address climate change is forecasted to lead to a demand supercycle for disruptive materials and acts as a massive tailwind.

But just how large is this expected level of demand to be? To answer this, we use two scenarios created by The International Energy Agency (IEA). The first is the Stated Policies Scenario, a more conservative model that assumes demand for material will double by 2040 relative to 2020 levels. Under this scenario, it’s assumed that society takes climate action in line with current and existing policies and commitments.

Then there is the Sustainable Development Scenario, which assumes more drastic action will take place to transform global energy use and meet international climate goals. Under this scenario, the demand for disruptive materials could rise as high as 300% relative to 2020 levels.

However, under both scenarios there’s still significant demand for each type of material.

| Disruptive Material | Stated Policies Scenario Demand Relative to 2020 | Sustainable Development Scenario Demand Relative to 2020 |

|---|---|---|

| Lithium | 13X | 42X |

| Graphite | 8X | 25X |

| Cobalt | 6X | 21X |

| Nickel | 7X | 19X |

| Manganese | 3X | 8X |

| Rare earth elements | 3X | 7X |

| Copper | 2X | 3X |

Overall, lithium is expected to see the most explosive surge in demand, as it could reach anywhere from 13 to 42 times the level of demand seen in 2020, based on the above scenarios.

Introducing the Global X Disruptive Materials ETF

The Global X Disruptive Materials ETF (Ticker: DMAT) seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the Solactive Disruptive Materials Index.

Investors can use this passively managed solution to gain exposure to the rising demand for disruptive materials and climate technologies.

我们在 2021 年开采的所有金属

这最初发布在 Elements上。注册 免费邮件列表, 每周在您的电子邮件中获得关于自然资源大趋势的精美可视化。

“如果不能种植,就必须开采”是一句名言,概括了矿物和金属在现代世界中的重要性。

从我们进入的每一栋建筑到我们使用的每一台设备,几乎我们周围的一切都含有一定数量的金属。

上图显示了 2021 年开采的所有 28 亿吨 金属,并使用美国地质调查局 ( USGS ) 的数据突出了每种金属的最大最终用途。

为什么我们开采这么多铁矿石?

2021 年,铁矿石 占 开采金属的 93% , 从地下开采了26 亿吨。值得注意的是,这是矿石产量,通常高于金属产量,因为金属是从矿石中提取和提炼的。例如,该矿石的铁金属含量估计为 16 亿吨。

| 金属/矿石 | 2021 年矿山产量(吨) | 占总数的百分比 |

|---|---|---|

| 铁矿 | 2,600,000,000 | 93.4% |

| 工业金属 | 181,579,892 | 6.5% |

| 技术和贵金属 | 1,474,889 | 0.05% |

| 全部的 | 2,783,054,781 | 100.0% |

98%的铁矿石转化 为生铁来炼钢,铁矿石在我们的生活中无处不在。 用铁矿石制成的钢铁 用于建筑、交通和家用电器,您可能每天都会遇到用它制成的东西,尤其是如果您住在城市里。

由于其在基础设施建设中的关键作用,铁矿石是支持城市化和经济增长的最重要材料之一。

工业金属

工业金属主要用于炼钢、建筑、化学制造和合金剂。2021 年,全球开采了超过 1.81 亿吨 这些金属。

| 工业金属 | 2021 年矿山产量(吨) | 占总数的百分比 |

|---|---|---|

| 铝* | 68,000,000 | 37.4% |

| 铬 | 41,000,000 | 22.6% |

| 铜 | 21,000,000 | 11.6% |

| 锰 | 20,000,000 | 11.0% |

| 锌 | 13,000,000 | 7.2% |

| 钛(精矿) | 9,000,000 | 5.0% |

| 带领 | 4,300,000 | 2.4% |

| 镍 | 2,700,000 | 1.5% |

| 锆矿物(锆石) | 1,200,000 | 0.7% |

| 镁* | 950,000 | 0.5% |

| 全部的 | 181,579,892 | 100.0% |

显示第 1 到 10 个条目,共 15 个条目

*代表精炼厂/冶炼厂的产量。

2021 年,铝占工业金属产量的近 40%。 中国是迄今为止最大的 铝生产国,占全球产量的一半以上。建筑业每年使用大约 25% 的铝,其中 23% 用于运输。

铬是一种鲜为人知的金属,在制造不锈钢方面起着关键作用。事实上,不锈钢通常含有 10% 至 30% 的铬,以增强其强度和耐腐蚀性。

铜、锰和锌是 2021 年开采的前五种工业金属,每种金属都有其独特的特性和在经济中的作用。

科技与贵金属

技术金属包括那些常用于技术和设备的金属。与工业金属相比,这些金属的开采规模通常较小,随着世界采用新技术,消费增长可能会更快。

| 科技与贵金属 | 2021 年矿山产量(吨) | 占总数的百分比 |

|---|---|---|

| 相信 | 300,000 | 20.3% |

| 钼 | 300,000 | 20.3% |

| 稀土氧化物 | 280,000 | 19.0% |

| 钴 | 170,000 | 11.5% |

| 钒 | 110,000 | 7.5% |

| 锂 | 106,000 | 7.2% |

| 钨 | 79,000 | 5.4% |

| 铌 | 75,000 | 5.1% |

| 银 | 24,000 | 1.6% |

| 镉 | 24,000 | 1.6% |

| 全部的 | 1,474,889 | 100.0% |

显示第 1 到 10 个条目,共 16 个条目

*代表精炼厂/冶炼厂的产量。

铼是生产方面最稀有的金属之一,主要用于制造对飞机和燃气涡轮发动机中的发动机涡轮叶片至关重要的超级合金。石油工业将其用于铼-铂催化剂中,以生产车用高辛烷值汽油。

在增长方面,清洁能源技术金属脱颖而出。例如, 自 2016 年以来,锂产量 翻了一番以上,势必会带动电动汽车电池制造的繁荣。同期,在磁铁需求上升的推动下,全球稀土产量翻了一番以上。

铟是这份名单上另一种有趣的金属。其中大部分用于制造氧化铟锡,这是触摸屏、电视屏幕和太阳能电池板的重要组成部分。

金属矿业大趋势

在过去的几十年里,世界的 物质消耗显着增长,经济增长和城市需要更多的资源。

与 1990 年代中期相比,全球铁矿石和铝产量增加了两倍多。其他金属,包括铜和钢,也出现了显着的消费增长。

如今,经济不仅在增长和城市化,而且还在采用 矿产密集型 清洁能源技术,这表明金属生产和消费将进一步增加。

破坏性材料的未来价值

简报会

到 2030 年,颠覆性材料的整体市场预计将超过 8000 亿美元

铜是最大的市场,而锂是增长最快的

破坏性材料的未来价值

一些选定的材料在下一代技术的扩展中发挥着关键作用。这可能会导致需求激增,从而导致每种材料的市场价值可能飙升。

这张来自 Global X ETF 的图表 仔细研究了 12 种颠覆性材料的预测市场价值,这些材料的气候投资越来越大。

飙升的市值

突出显示的材料 各自都是价值十亿美元的市场。但哪个具有最大的预计未来市场价值?

铜是该组中最大和最成熟的市场之一。因此,预计复合年增长率 (CAGR) 较低。

然而,当谈到增长最快的市场时,锂在 2021 年至 2028 年的预测期内以超过 23% 的复合年增长率占据主导地位。锂是用于电动汽车和其他地方的锂离子电池的重要 成分 。

| 破坏性材料 | 预计市场价值 ($B) | CAGR(预测期内) |

|---|---|---|

| 铜 | 到 2029 年 $394.0B | 4.2% (2021-2029年) |

| 锂 | 到 2028 年 $191.0B | 23.3% (2021-2028年) |

| 镍 | 到 2028 年 $59.0B | 7.3% (2021-2028年) |

| 锌 | 到 2027 年 $49.6B | 4.0% (2021-2027年) |

| 锰 | 到 2027 年 $42.0B | 7.4% (2019-2027P) |

| 钴 | 到 2029 年 $17.3B | 12.5% (2021-2029年) |

| 稀土金属 | 到 2030 年 $15.4B | 9.1% (2021-2030P) |

| 铂 | 到 2027 年 $9.6B | 5.0% (2020-2027年) |

| 碳纤维 | 到 2030 年 $9.0B | 9.2% (2022-2030P) |

| 碳材料 | 到 2027 年 $8.7B | 6.8% (2020-2027年) |

| 钯 | 到 2028 年 $5.6B | 4.6% (2022-2028P) |

| 石墨烯 | 到 2028 年 $1.3B | 16.2% (2022-2028年) |

到本十年末,这些顶级材料的总市值预计将超过 8000 亿美元。在随后的几年中,随着应对气候变化的努力加速,这些材料的总价值很可能达到 1 万亿美元。

您应该投资破坏性材料吗?

您应该投资破坏性材料吗?

新技术正在对交通和能源部门产生变革性影响。随着这些技术的发展,越来越明显的是,一小部分材料、金属和矿物(统称为颠覆性材料)是创新所需的关键组成部分。

这张来自 Global X ETF 的图表 仔细研究了对推动气候技术至关重要的颠覆性材料。随着全球脱碳努力的不断加强,颠覆性材料可能会进入需求超级周期,其特征是长达数十年的结构性需求增长和价格上涨。

未来的基石

特别是有 10 类颠覆性材料,预计它们的需求增长将作为它们在新兴技术中的作用的一部分。

| 破坏性材料 | 适用性 |

|---|---|

| 锌 | 通过称为镀锌的过程保护金属表面不生锈。这对风能至关重要。 |

| 钯和铂 | 通常用于催化转化器,因此在氢燃料电池技术中发挥着重要作用。 |

| 镍 | 一种耐腐蚀金属,用于使其他金属更耐用。 |

| 锰 | 电池和钢铁生产所需的重要矿物。 |

| 锂 | 锂离子电池的基本组成部分。 |

| 石墨烯 | 已知最薄的材料,强度也是钢的 100 倍。用于传感器和晶体管。 |

| 稀土材料 | 更广泛的类别,包括 15 种镧系元素以及钇。这些金属存在于所有类型的电子产品中。 |

| 铜 | 可靠的电导体。它还可以杀死细菌,使其在大流行期间很有用。 |

| 钴 | 可充电锂电池的重要成分,仅在世界特定地区发现。 |

| 碳纤维与碳材料 | 用于航空航天和汽车工业的坚固轻质材料。 |

虽然这 10 个类别并不构成整个颠覆性物质世界,但它们对于确保气候和技术先进的未来都是必不可少的。

绿色革命如何改变材料市场

有关全球气温上升和极端天气事件的数据令人震惊, 世界各地的政府和组织都在加大努力,通过新的预算和政策来应对其影响。

以美国气候灾害总数飙升为例。最近一次是在 2021 年, 天气灾害的数量 为 20 次,而在 1980 年,这一数字要小得多,只有 3 次。此外, 每年的总灾难成本已超过1000 亿美元。

在全球范围内,2021 年十大 最 极端 的天气 事件造成了 1700 亿美元 的损失。

| 秩 | 气候事件 | 成本(美元) |

|---|---|---|

| #1 | 飓风艾达 | $65.0B |

| #2 | 欧洲洪水 | $43.0B |

| #3 | 德州冬季风暴 | $23.0B |

| #4 | 河南洪水 | $17.6B |

| #5 | 不列颠哥伦比亚省洪水 | $7.5B |

| #6 | 法国“寒潮” | $5.6B |

| #7 | 旋风亚斯 | $3.0B |

| #8 | 澳大利亚洪水 | $2.1B |

| #9 | 台风英法 | $2.0B |

| #10 | 旋风塔克泰 | $1.5B |

更重要的是,一些研究估计,这些不断上升的成本远未停止。到 2050 年,每年因天气灾害造成的损失可能会 飙升至1 万亿美元 以上 。为了减缓气温上升,各国政府正在大幅增加气候支出。例如,美国将在未来五年内每年花费 800 亿美元。

要了解气候支出如何影响材料市场,请考虑典型太阳能电池板背后的复杂性,它需要近 20 种 不同的材料,包括用于布线的铜、用于半导体的硼和磷,以及用于框架的锌和镁。

总的来说,这些材料对于锂电池、太阳能电池板、风力涡轮机、燃料电池、机器人技术和 3D 打印机等各种新兴技术的扩展至关重要。因此,正在转化为对使应对气候变化成为可能的破坏性材料的更高水平的需求。

预计到 2040 年破坏性物质增长

预计我们应对气候变化方式的社会转变 将导致对破坏性材料的需求超级周期,并成为巨大的顺风。

但这种预期的需求水平究竟有多大?为了回答这个问题,我们使用了 国际能源署 (IEA) 创建的两个情景。第一个是 既定政策情景,这是一个更保守的模型,假设材料需求到 2040 年将比 2020 年水平翻一番。在这种情况下,假设社会根据当前和现有的政策和承诺采取气候行动。

然后是 可持续发展情景,假设将采取更严厉的行动来改变全球能源使用并实现国际气候目标。在这种情况下,对颠覆性材料的需求可能会比 2020 年的水平高出 300% 。

然而,在这两种情况下,对每种材料的需求仍然很大。

| 破坏性材料 | 相对于 2020 年的既定政策情景需求 | 相对于2020年的可持续发展情景需求 |

|---|---|---|

| 锂 | 13X | 42X |

| 石墨 | 8X | 25X |

| 钴 | 6X | 21X |

| 镍 | 7X | 19X |

| 锰 | 3X | 8X |

| 稀土元素 | 3X | 7X |

| 铜 | 2X | 3X |

总体而言,锂的需求预计将出现最爆炸性的激增,因为根据上述情景,它可能达到 2020 年需求水平的 13 至 42 倍。

推出 Global X Disruptive Materials ETF

Global X Disruptive Materials ETF(股票代码:DMAT)旨在提供与 Solactive Disruptive Materials Index 的价格和收益表现(扣除费用和支出之前)大体对应的投资结果。

投资者可以使用这种被动管理的解决方案来了解对颠覆性材料和气候技术不断增长的需求。

您应该投资破坏性材料吗?

新技术正在对交通和能源部门产生变革性影响。随着这些技术的发展,越来越明显的是,一小部分材料、金属和矿物(统称为颠覆性材料)是创新所需的关键组成部分。

这张来自 Global X ETF 的图表 仔细研究了对推动气候技术至关重要的颠覆性材料。随着全球脱碳努力的不断加强,颠覆性材料可能会进入需求超级周期,其特征是长达数十年的结构性需求增长和价格上涨。

未来的基石

特别是有 10 类颠覆性材料,预计它们的需求增长将作为它们在新兴技术中的作用的一部分。

| 破坏性材料 | 适用性 |

|---|---|

| 锌 | 通过称为镀锌的过程保护金属表面不生锈。这对风能至关重要。 |

| 钯和铂 | 通常用于催化转化器,因此在氢燃料电池技术中发挥着重要作用。 |

| 镍 | 一种耐腐蚀金属,用于使其他金属更耐用。 |

| 锰 | 电池和钢铁生产所需的重要矿物。 |

| 锂 | 锂离子电池的基本组成部分。 |

| 石墨烯 | 已知最薄的材料,强度也是钢的 100 倍。用于传感器和晶体管。 |

| 稀土材料 | 更广泛的类别,包括 15 种镧系元素以及钇。这些金属存在于所有类型的电子产品中。 |

| 铜 | 可靠的电导体。它还可以杀死细菌,使其在大流行期间很有用。 |

| 钴 | 可充电锂电池的重要成分,仅在世界特定地区发现。 |

| 碳纤维与碳材料 | 用于航空航天和汽车工业的坚固轻质材料。 |

虽然这 10 个类别并不构成整个颠覆性物质世界,但它们对于确保气候和技术先进的未来都是必不可少的。

绿色革命如何改变材料市场

有关全球气温上升和极端天气事件的数据令人震惊, 世界各地的政府和组织都在加大努力,通过新的预算和政策来应对其影响。

以美国气候灾害总数飙升为例。最近一次是在 2021 年, 天气灾害的数量 为 20 次,而在 1980 年,这一数字要小得多,只有 3 次。此外, 每年的总灾难成本已超过1000 亿美元。

在全球范围内,2021 年十大 最 极端 的天气 事件造成了 1700 亿美元 的损失。

| 秩 | 气候事件 | 成本(美元) |

|---|---|---|

| #1 | 飓风艾达 | $65.0B |

| #2 | 欧洲洪水 | $43.0B |

| #3 | 德州冬季风暴 | $23.0B |

| #4 | 河南洪水 | $17.6B |

| #5 | 不列颠哥伦比亚省洪水 | $7.5B |

| #6 | 法国“寒潮” | $5.6B |

| #7 | 旋风亚斯 | $3.0B |

| #8 | 澳大利亚洪水 | $2.1B |

| #9 | 台风英法 | $2.0B |

| #10 | 旋风塔克泰 | $1.5B |

更重要的是,一些研究估计,这些不断上升的成本远未停止。到 2050 年,每年因天气灾害造成的损失可能会 飙升至1 万亿美元 以上 。为了减缓气温上升,各国政府正在大幅增加气候支出。例如,美国将在未来五年内每年花费 800 亿美元。

要了解气候支出如何影响材料市场,请考虑典型太阳能电池板背后的复杂性,它需要近 20 种 不同的材料,包括用于布线的铜、用于半导体的硼和磷,以及用于框架的锌和镁。

总的来说,这些材料对于锂电池、太阳能电池板、风力涡轮机、燃料电池、机器人技术和 3D 打印机等各种新兴技术的扩展至关重要。因此,正在转化为对使应对气候变化成为可能的破坏性材料的更高水平的需求。

预计到 2040 年破坏性物质增长

预计我们应对气候变化方式的社会转变 将导致对破坏性材料的需求超级周期,并成为巨大的顺风。

但这种预期的需求水平究竟有多大?为了回答这个问题,我们使用了 国际能源署 (IEA) 创建的两个情景。第一个是 既定政策情景,这是一个更保守的模型,假设材料需求到 2040 年将比 2020 年水平翻一番。在这种情况下,假设社会根据当前和现有的政策和承诺采取气候行动。

然后是 可持续发展情景,假设将采取更严厉的行动来改变全球能源使用并实现国际气候目标。在这种情况下,对颠覆性材料的需求可能会比 2020 年的水平高出 300% 。

然而,在这两种情况下,对每种材料的需求仍然很大。

| 破坏性材料 | 相对于 2020 年的既定政策情景需求 | 相对于2020年的可持续发展情景需求 |

|---|---|---|

| 锂 | 13X | 42X |

| 石墨 | 8X | 25X |

| 钴 | 6X | 21X |

| 镍 | 7X | 19X |

| 锰 | 3X | 8X |

| 稀土元素 | 3X | 7X |

| 铜 | 2X | 3X |

总体而言,锂的需求预计将出现最爆炸性的激增,因为根据上述情景,它可能达到 2020 年需求水平的 13 至 42 倍。

推出 Global X Disruptive Materials ETF

Global X Disruptive Materials ETF(股票代码:DMAT)旨在提供与 Solactive Disruptive Materials Index 的价格和收益表现(扣除费用和支出之前)大体对应的投资结果。

投资者可以使用这种被动管理的解决方案来了解对颠覆性材料和气候技术不断增长的需求。