-

1

-

2

-

3

}In the budgeting chapter we looked at the preparation of budgets within an organisation.These budgets were prepared at a total level and became a target against which actual results could be measured.

}In this standard costing chapter we will look at another control technique known as standard costing.

}Standard costing also produces a target against which we can measure actual results, but in standard costing the targets are set at a unit level.

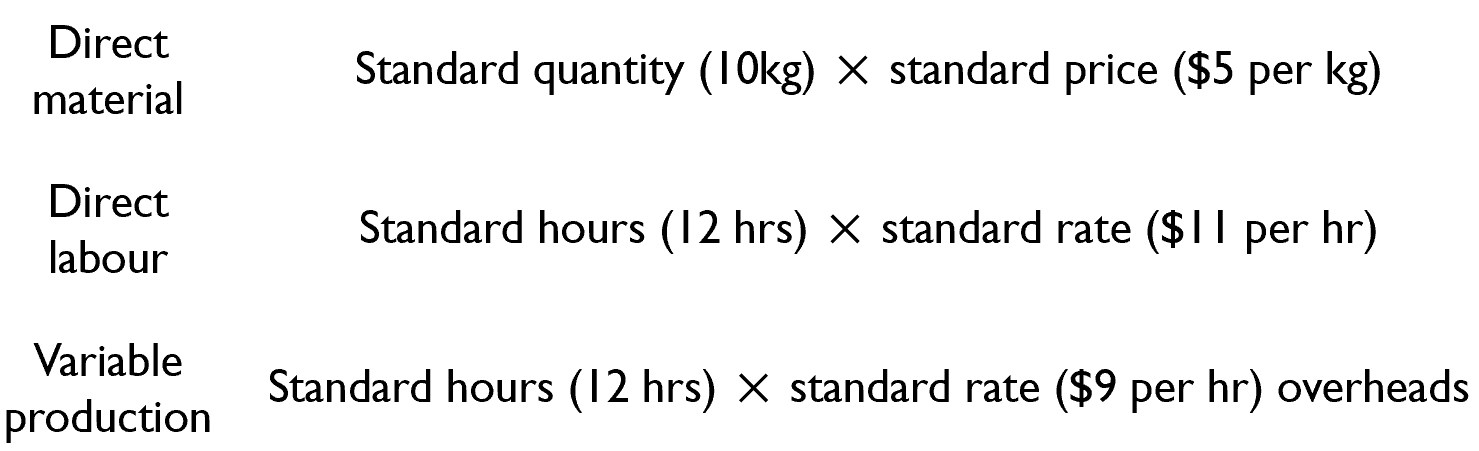

Standard cost

}A standard cost is a carefully pre-determined unit cost which is prepared for each cost unit.

}The standard becomes a target against which performance can be measured.

}The actual costs incurred are measure dafter the event and compared to the pre-determined standards.

}The difference between the standard andthe actual is known as a variance.

}Analysing variances can help managers focus on the areas of the business requiring the most attention.

}This is known as management by exception.