-

1

-

2

}Process costing is the costing method applicable where goods or services result from a sequence of continuous orrepetitive operations or processes.

}Process costing is used when a company is mass producing the same item and the item goes through anumber of different stages.

}Process costing is an example of continuous operation costing.

}Examples include the chemical, cement, oil refinery, paint, breweries and textile industries.

}One of the features of process costing is that in most process costing environments the products are identical and indistinguishable from each other.

}For this reason, an average cost per unitis calculated for each process.

Average cost per unit =Net costs of inputs/Expected output

}Expected output is what we expect to getout of the process.

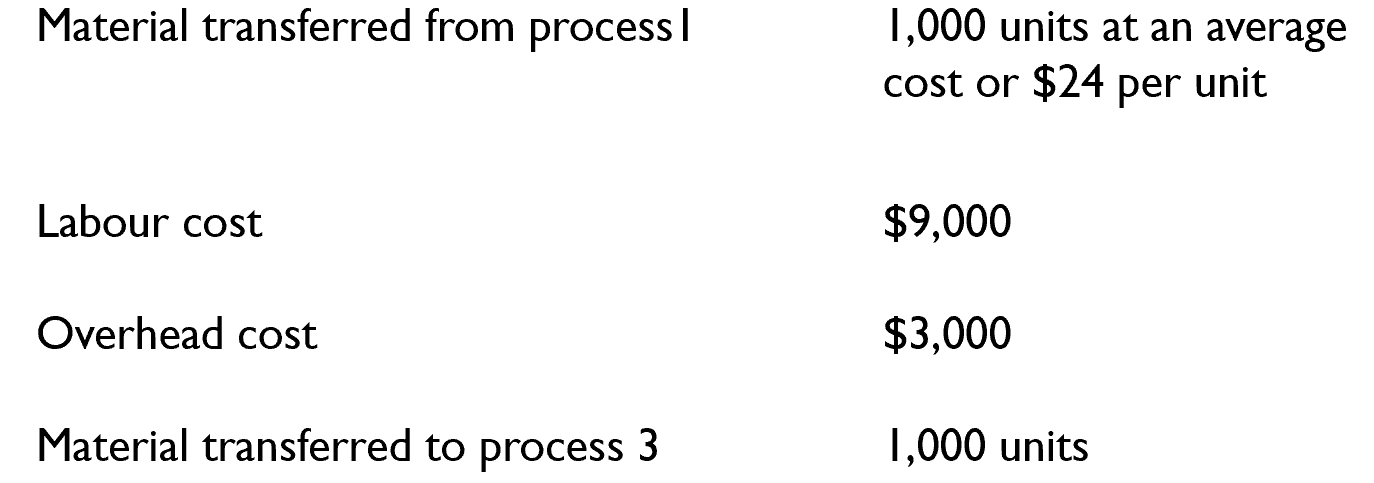

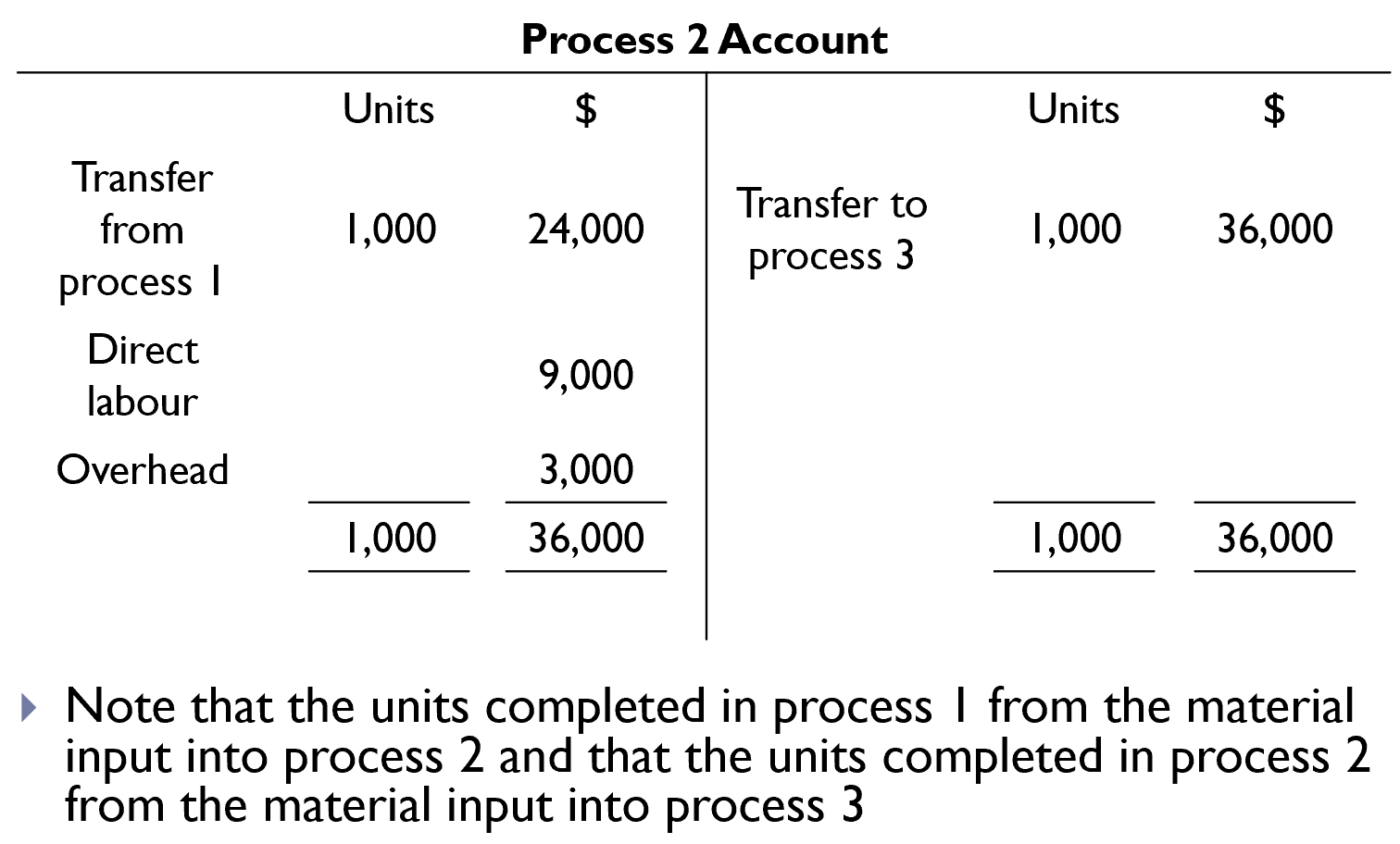

}Another feature of process costing is that the output of one process forms the material input of the next process.

}When there is closing work-in-progress(WIP) at the end of one period, this forms the opening WIP at the beginning ofthe next period.

}The details of process costs and units are recorded in a process account which shows the materials, labour and overheads input to the process and the materials output at the end of the process.