The treatment of fixed production costs

上一节

下一节

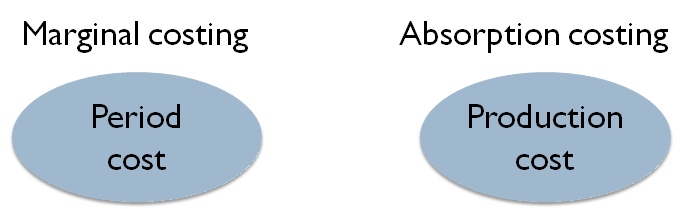

Marginal and absorption costing are two different ways of valuing the cost of goods sold and finished goods in inventory which can affect the profit charged to the statement of profit orloss.

The main difference between marginal costing and absorption costing is the treatment of fixed production costs:

Marginal costing only assigns variable productions overheads to each unit.

Fixed production overheads are treated asperiod costs.

Period costs are costs which are charged in full to the statement of profit or loss in the period in which they are incurred.

Absorption costing assigns both the fixed and variable production overheads to each unit

Product costs are charged to the individual product and matched against the sales revenue they generate.