Learning objectives/ 学习目标

上一节

下一节

Learning objectives

Understand the use of continuous and period end inventory records.

Calculatethe value of closing inventory using 'first in, first out' and 'average cost'.

Recognise the need for adjustments forinventory in preparing financial statements.

Record opening and closing inventory.

Recognise which costs should be included in valuing inventories.

Identify the alternative methods of valuing inventory.

Understand and apply the IASB requirements for valuing inventories.

Understand the impact of accounting conceptsonthe valuation of inventory.

Identify the impactof inventory valuation methodson profit and on assets.

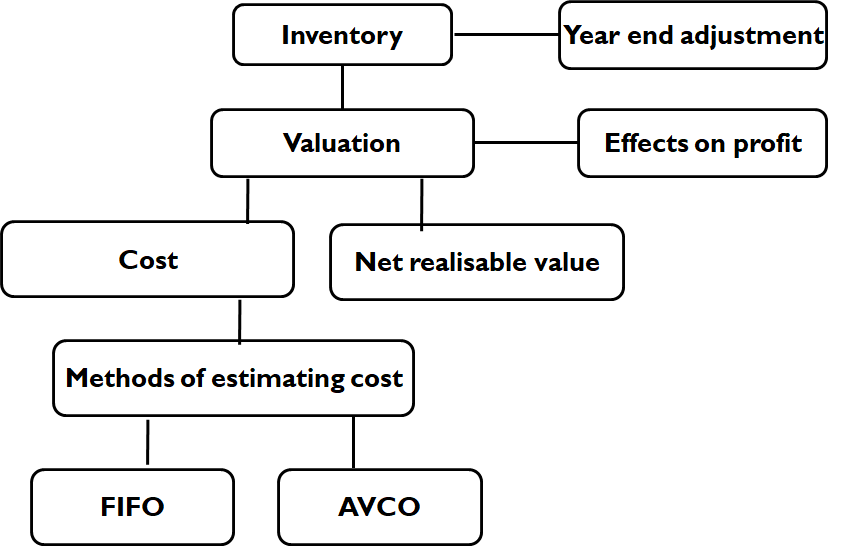

Overview