Syllabus/ 课程大纲

下一节

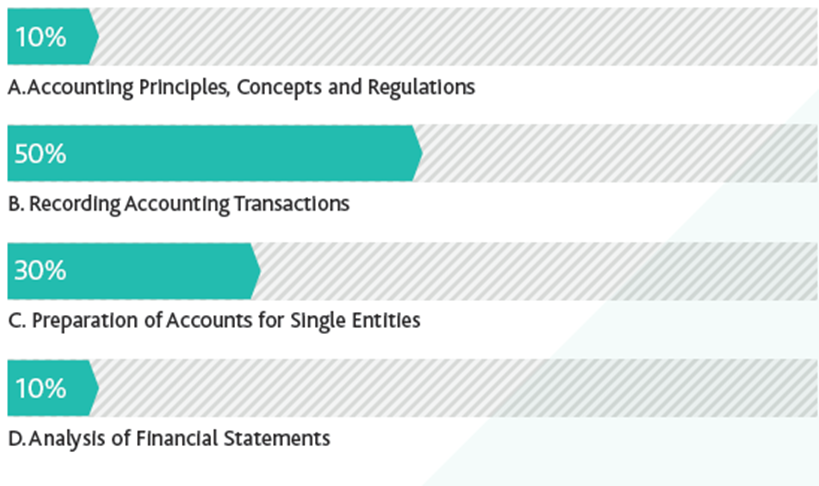

Aim and Purpose

Themain objective of this subject is to obtain a practical understanding offinancial accounting and the process behind the preparation of financialstatements for single entities.

These statements are prepared within a conceptual and regulatory framework requiringan understanding of the role of legislation and of accounting standards. Theneed to understand and apply necessary controls for accounting systems, and thenature of errors is also covered. There is an introduction to measuringfinancial performance with the calculation of basic ratios.